- +91 9879209079

-

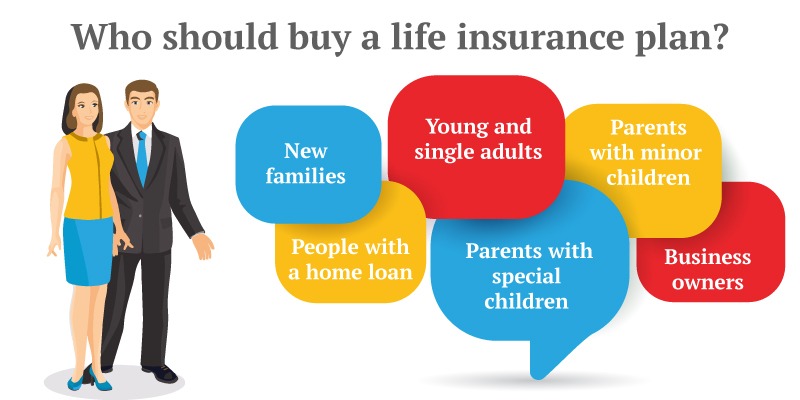

Life insurance is a contract between an individual (policyholder) and an insurance company, where the insurer promises to pay a designated sum of money (the death benefit) to the beneficiaries of the policy upon the death of the insured person. In exchange for this coverage, the policyholder pays regular premiums to the insurance company.

The primary purpose of life insurance is to provide financial protection and support to the family or dependents of the insured in the event of their death. It helps ensure that the beneficiaries are financially taken care of and can cover various expenses such as funeral costs, outstanding debts, living expenses, education expenses, and other financial obligations.

Life insurance policies come in various types, such as term life insurance, whole life insurance, universal life insurance, and others, each offering different features and benefits. Choosing the right type of life insurance depends on individual needs, financial goals, and budgetary considerations.

Life insurance offers several benefits that can provide financial security and peace of mind for both the policyholder and their beneficiaries. Some of the key benefits of life insurance include:

It's essential to carefully consider your financial needs, long-term goals, and family situation when choosing a life insurance policy. Life insurance can play a vital role in providing financial security and protection for your loved ones in times of need. Consulting with a financial advisor can help you select the most suitable life insurance coverage for your specific circumstances.

302-Shubham Complex, Near Anand

Hospital, Opposite Kailash Sweets,

Nanpura Surat - 395001

+91 9879209079

+91 9503019880

+91 9879766866

Risk Factors – Investments in Mutual Funds are subject to Market Risks. Read all scheme related documents carefully before investing. Mutual Fund Schemes do not assure or guarantee any returns. Past performances of any Mutual Fund Scheme may or may not be sustained in future. There is no guarantee that the investment objective of any suggested scheme shall be achieved. All existing and prospective investors are advised to check and evaluate the Exit loads and other cost structure (TER) applicable at the time of making the investment before finalizing on any investment decision for Mutual Funds schemes. We deal in Regular Plans only for Mutual Fund Schemes and earn a Trailing Commission on client investments. Disclosure For Commission earnings is made to clients at the time of investments.

AMFI Registered Mutual Fund Distributor – ARN-156112 | Date of initial registration – 25-Apr-2024 | Current validity of ARN – 01-Jul-2027

Important Links | Disclaimer | Disclosure | Privacy Policy | SID/SAI/KIM | Code of Conduct | SEBI Circulars | AMFI Risk Factors